Creating a legally sound and secure promissory note is a critical step in any business relationship. It's a document outlining the terms of a loan, establishing a clear framework for repayment, and protecting both the lender and the borrower. A properly drafted secured promissory note provides a robust defense against potential legal disputes and ensures a smooth and reliable financial transaction. This article will delve into the essential components of a secured promissory note, offering guidance on its creation and the importance of professional legal counsel. Secured Promissory Note Template – understanding its nuances is paramount for anyone involved in lending or borrowing. This guide aims to provide a comprehensive overview, equipping you with the knowledge to create a document that safeguards your interests.

Understanding the Core Components of a Secured Promissory Note

A secured promissory note is a legally binding agreement where a borrower pledges collateral to secure a loan. This collateral serves as a guarantee for the lender, reducing the risk of loss if the borrower defaults on the loan. The specific collateral can vary widely, ranging from real estate to equipment or even intellectual property. The secured nature of the note significantly strengthens the lender's position and provides a valuable safety net. A well-structured note clearly defines the terms of the loan, including the principal amount, interest rate, repayment schedule, and consequences of default. It's crucial to consult with a legal professional to ensure the note complies with all applicable laws and regulations.

The fundamental elements of a secured promissory note typically include:

- Parties Involved: Clearly identify the borrower, lender, and any other relevant parties involved in the loan agreement.

- Loan Amount: Specify the exact amount of money being borrowed.

- Interest Rate: Define the interest rate charged on the loan, whether fixed or variable.

- Repayment Schedule: Outline the frequency and amount of payments, including the due date for each payment.

- Collateral: Detail the specific assets pledged as collateral, including their value and condition.

- Default Provisions: Clearly state the consequences of a borrower failing to meet their repayment obligations.

- Governing Law: Specify the jurisdiction whose laws will govern the interpretation and enforcement of the note.

The Importance of a Detailed and Comprehensive Template

While a generic template can be a starting point, a truly effective secured promissory note requires careful customization to reflect the specific circumstances of the loan. A detailed template allows for clarity and minimizes the potential for misunderstandings. It's vital to consider the borrower's industry and the nature of the loan when drafting the note. For example, a note for a construction project will require different terms than a note for a business loan. Furthermore, incorporating clauses addressing potential disputes and remedies is essential.

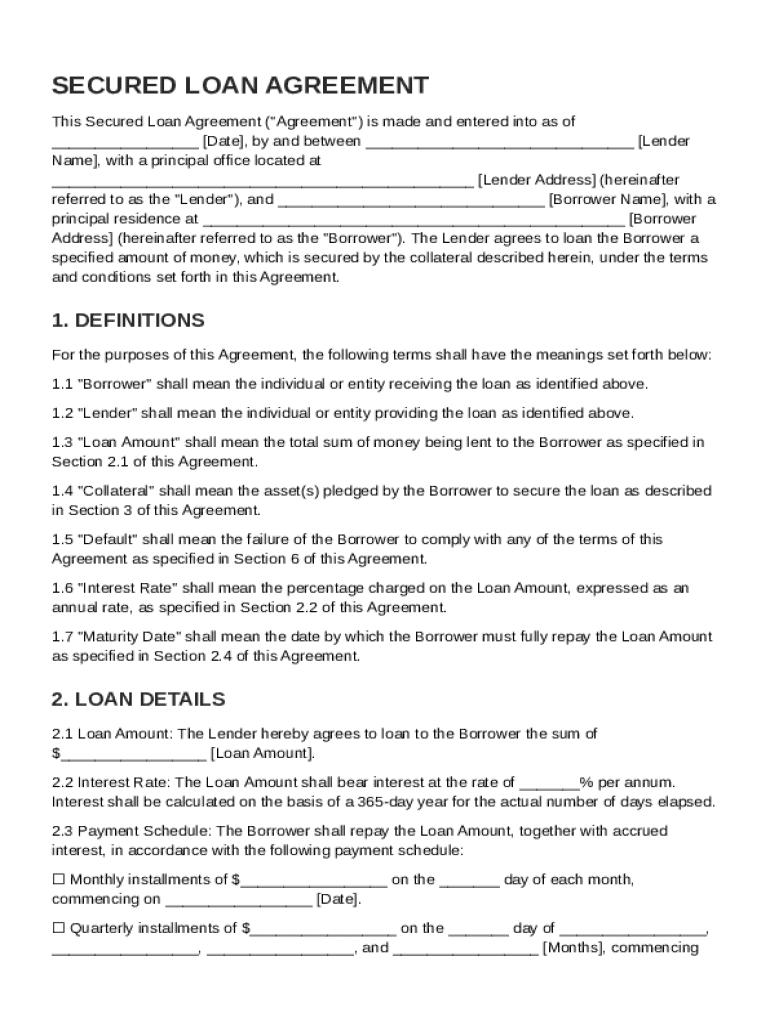

Section 1: Borrower Information

This section provides essential details about the borrower, including their legal name, address, and contact information. It's important to accurately represent the borrower's identity to avoid potential legal challenges. The lender should verify the borrower's legal existence and ensure they have the authority to enter into the loan agreement. A clear statement of the borrower's business structure (e.g., sole proprietorship, partnership, corporation) is also beneficial.

Section 2: Lender Information

This section details the lender's information, including their legal name, address, and contact information. The lender should also provide details about their financial stability and experience in lending. It's crucial to establish a clear relationship between the lender and the borrower, fostering trust and transparency. A statement confirming the lender's commitment to responsible lending practices is highly recommended.

Section 3: Loan Details

This is the core of the note, outlining the specifics of the loan. It should include:

- Principal Amount: The initial amount of money being borrowed.

- Interest Rate: The annual interest rate charged on the loan.

- Loan Term: The length of time the loan is to be repaid (e.g., 5 years, 10 years).

- Repayment Schedule: A detailed breakdown of each payment, including the amount, due date, and frequency. Consider using a schedule that aligns with the borrower's business cycle.

- Collateral Description: A precise description of the collateral pledged, including its value and condition. A professional appraisal may be required.

Section 4: Default Provisions

This section outlines the consequences of a borrower's failure to meet their repayment obligations. It's crucial to clearly define the remedies available to the lender in the event of default, such as acceleration of the loan, seizure of collateral, and legal action. The terms of default should be clearly stated and legally enforceable.

Section 5: Governing Law and Dispute Resolution

This section specifies the jurisdiction whose laws will govern the interpretation and enforcement of the note. It may also include a dispute resolution mechanism, such as mediation or arbitration, to resolve any disagreements between the borrower and lender. Choosing a jurisdiction with favorable legal protections can be beneficial.

Securing the Collateral: A Critical Consideration

The value and security of the collateral are paramount. A robust collateral agreement should clearly define the terms of the collateral, including its condition, valuation, and insurance coverage. It's advisable to engage a qualified appraisal to determine the fair market value of the collateral. The lender should also obtain adequate insurance to protect the collateral against loss or damage. Proper documentation and record-keeping are essential to demonstrate the security of the collateral. Consider including a clause specifying the lender's right to seize and sell the collateral if the borrower defaults.

The Role of Legal Counsel

Drafting a secured promissory note is a complex legal process. It's strongly recommended that borrowers consult with an experienced attorney to ensure the note complies with all applicable laws and regulations. An attorney can help navigate the intricacies of the agreement, protect your interests, and minimize the risk of disputes. They can also advise on the appropriate collateral and ensure the note is properly executed. The attorney can also assist with negotiating the terms of the note with the lender.

Conclusion

A secured promissory note is a powerful tool for securing loans and fostering strong financial relationships. By carefully considering the key components, tailoring the template to the specific circumstances, and seeking professional legal guidance, borrowers can create a document that provides a robust and reliable framework for repayment. Remember that a well-drafted note is an investment in your financial future. Proper planning and execution are essential for maximizing the benefits and minimizing the risks associated with borrowing. Ultimately, a secure promissory note serves as a vital safeguard for both the lender and the borrower, promoting stability and trust within the lending relationship. Secured Promissory Note Template – a solid foundation for a successful financial transaction.

0 Response to "Secured Promissory Note Template"

Posting Komentar